- Malling.no/

- Blogg/

- Savills on rent watch as world city risk changes

Savills on rent watch as world city risk changes

Marianne har jobbet som markedssjef i Malling & Co siden 2010. Hun er glødende opptatt av merkevarebygging basert på samspillet mellom markedsføring, CRM og ny teknologi. Marianne har over 25 års erfaring med markedsføring av næringseiendom men er utdannet profesjonell dykker og er verdens første kvinnelige metningsdykker. Når hun ikke tenker på markedsføring, er hun engasjert i byutvikling, ny teknologi og kultur.

Established world city real estate markets are going to see lower capital growth in the next decade as interest rates rise, so income will be the key reason for investing, according to international real estate advisor Savills.

In its new flagship publication, Impacts: the future of global real estate, Savills says risk needs to be measured differently, as security and scale of income becomes the major driver. The firm identifies cities which are resource rich, young and fast-growing, economic powerhouses or at low risk of natural disasters as ones to watch for the next decade. According to the report, the ability of cities to attract people and talent pools will be a key indicator of income security in the next 10 years.

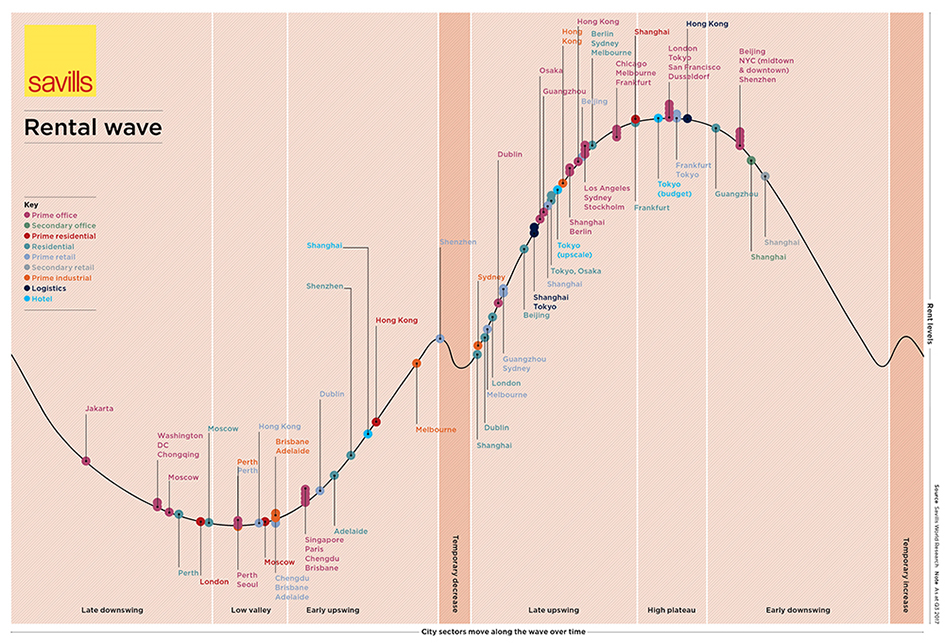

Savills has analysed rental growth in different real estate sectors in world cities and plotted where each stands on the new Savills rental wave. It identifies cities and sectors which investors may want to take look at more closely for security of income and potential rental growth.

- Prime office growth has been highest in San Francisco (+99%), Shenzhen and Beijing (both +71%) and London West End (+69%) since 2008. This leaves these city sectors near the top of the rental curve: in late upswing, on a high plateau or in early downswing.

- In Singapore, double digit falls have been seen in prime offices (-26%), residential (-25%) and prime retail (-15%), leaving these sectors in or near the trough of the rental wave.

- Hotels in Shanghai, prime industrial in Melbourne and Shenzhen residential are examples of early-stage rental growth in the current cycle suggesting further potential, but investors may face tough competition and high prices for assets in these markets.

- Shenzhen has experienced the most rental growth in residential since the end of 2008 (+82%).

- New and growing economic powerhouse Jakarta is near the end of the late downswing phase of the cycle and potentially offers high rental growth, but with the greater risk of a young market in an emerging economy.

- Established investment classes in world cities, e.g. prime offices in cities like London, Tokyo and San Francisco are at the top of the wave but may offer a safe harbour for investors as rents could remain on a ‘high plateau’ for some time.

“If the fifty years of real estate investment before 2007 were about capital growth and the post GFC decade about survival and riding the recovery, the next ten years and beyond will be about security of income in a low interest rate world, with investors increasingly shifting their focus towards rental markets in world cities”, says Yolande Barnes, head of Savills World Research.

“Whether investors are looking for capital growth or stable income streams, the behaviour of rental markets is key”, says Barnes. “Rents don’t lie; they’re a function of two market fundamentals: occupier demand – put simply, where people want to be - and supply conditions. In many global investment markets, there is very little scope for further yield compression so capital growth can only come with rental growth.”

Investment funds are increasingly focused on how to pay pensions to ageing populations in advanced countries. This is a permanent shift, made more urgent in a low inflation, low interest rate era, and increases focus on the quality of income, says Savills. By contrast, in more emerging economies, notably across China, investors are still in the phase of needing to grow portfolios, so can take advantage of growth opportunities in riskier markets. Investors need to understand the risks posed by economic trends, new technology, social change, natural threats and resource scarcity, and how these impact different real estate sectors at a city, as well as world region, level.

Savills Rental Wave – understanding where cities sit in the rental cycle:

The report introduces the Savills Rental Wave, which describes all possible stages of rental growth. Cities in the ‘early upswing’ are described as ones for investors to watch as they have scope for further rental growth, but Savills warns that intense competition for stock may lead to yield compression and high prices in some locations, while others are difficult for international investors to access.

On the basis of rental growth alone, Singapore appears poised for investment in many sectors, Jakarta and Perth in prime offices, Shenzhen for residential and prime retail, Shanghai for hotels, and Melbourne for prime industrial, but some of these cities are expensive and some sectors have already seen heavy investor activity pushing yields down.

Singapore prime office rents are still on average -26% below their 2007 level, says Savills, but Chinese investor demand for Singaporean assets has continued to suppress yields. Investor appetite reflects the expectation that the city could potentially become the region’s lead economic powerhouse.

Many core, world city residential real estate markets are heavily concentrated in the ‘late upswing’ phase, including London mainstream, Berlin, Sydney, Melbourne, Beijing and Tokyo, while Frankfurt and Shanghai are on the cusp of a ‘high plateau’. In this group, the highest residential rental growth of the past ten years has been in mainstream residential lettings in Shanghai (59%) and Sydney (57%) while European listings have also been strong since 2008, with Berlin up 53% and Frankfurt up 42%.

Cities, sectors and growth on the Savills Rental Wave

Source: Savills World Research

A high plateau positioning should not necessarily discourage investors, Savills says. The combination of economic stronghold and relative economic and political stability can augur well for those more concerned with stable and secure incomes than rental-driven capital growth in sectors such as prime offices in London, Tokyo and San Francisco or budget hotels and retail in Tokyo.

By contrast, high rental growth prospects likely come with far greater risk, for example Jakarta (where the metro population is forecast to exceed Tokyo’s by 2027, but whose real estate markets are still small and relatively immature on the world stage) or Shenzhen which is relatively inaccessible to many foreign investors but one of the most youthful and fast growing cities in the world.

“To correctly understand real estate risk, it’s imperative that investors understand markets at a city, and even a neighbourhood level and how that applies to each individual real estate sector. Rental growth prospects do not necessarily indicate a ‘buy’ status, particularly if the price is too high, or if an injection of new supply could tip a sector into oversupply and a rental double-dip,” continues Barnes.

Youthful cities tipped for growth

Understanding social change is essential. Cities with youthful populations are more likely to be centres of higher education, magnets for skilled migration and catalysts for innovation and economic growth. Rental growth will follow, Savills says.

The firm has earmarked key cities in each world region where the Gen Z (15-34 year olds in 2027) to Gen X (50-69 year olds in 2027) ratio is forecast to be highest within the next decade, which include Shenzhen, Jakarta, Auckland and Austin.

Savills cities to watch – measuring future occupier risk:

Cities which rank as ‘economic powerhouse’ or ‘youthful’ are likely to offer a substantial variety of future opportunities for investors, says Jeremy Bates, head of Savills Worldwide Occupier Services. “The biggest asset in any nation’s economy is its people. But competition is intense for talented workforces in developed countries with ageing populations, while emerging economies are nurturing an increasing number of young people.

“New generations will drive occupier demand for certain types of buildings and locations. This will potentially lead to a shift in what constitutes a quality ‘covenant’ with buildings let on short leases to a deep pool of small local businesses potentially finding the most favour with investors as sources of reliable income.”

Download the full report by clicking the image below:

For further information please contact:

Haakon Ødegaard, Head of Malling & Co Research and Valuation Mobil: +47 938 14 645

Yolande Barnes, Savills world research Tel: +44 (0) 20 7409 8899

Jeremy Bates, Savills worldwide occupier services Tel: +44 (0) 20 7409 8813

Sue Laming, Savills press office Tel: +44 (0) 20 7016 3802

Natalie Moorse, Savills press office Tel: +44 (0) 20 7075 2827